Bullish Options Positioning Sets High Bar for This Week’s Earnings

MICHAEL KRAMER AND THE CLIENTS OF MOTT CAPITAL OWN AAPL, MSFT, AMZN

This week will be one of the busiest of 2025, with numerous earnings reports and significant economic data releases. That will only add to the daily rounds of volatility we’re already experiencing surrounding tariff news. The economic data for April should start shedding light on the potential fallout from the Liberation Day tariff announcement, while earnings results from Apple, Microsoft, Meta, and Amazon will offer further insights into how severe that fallout might become.

Positioning ahead of these earnings appears surprisingly bullish, especially for the four mega-cap stocks.

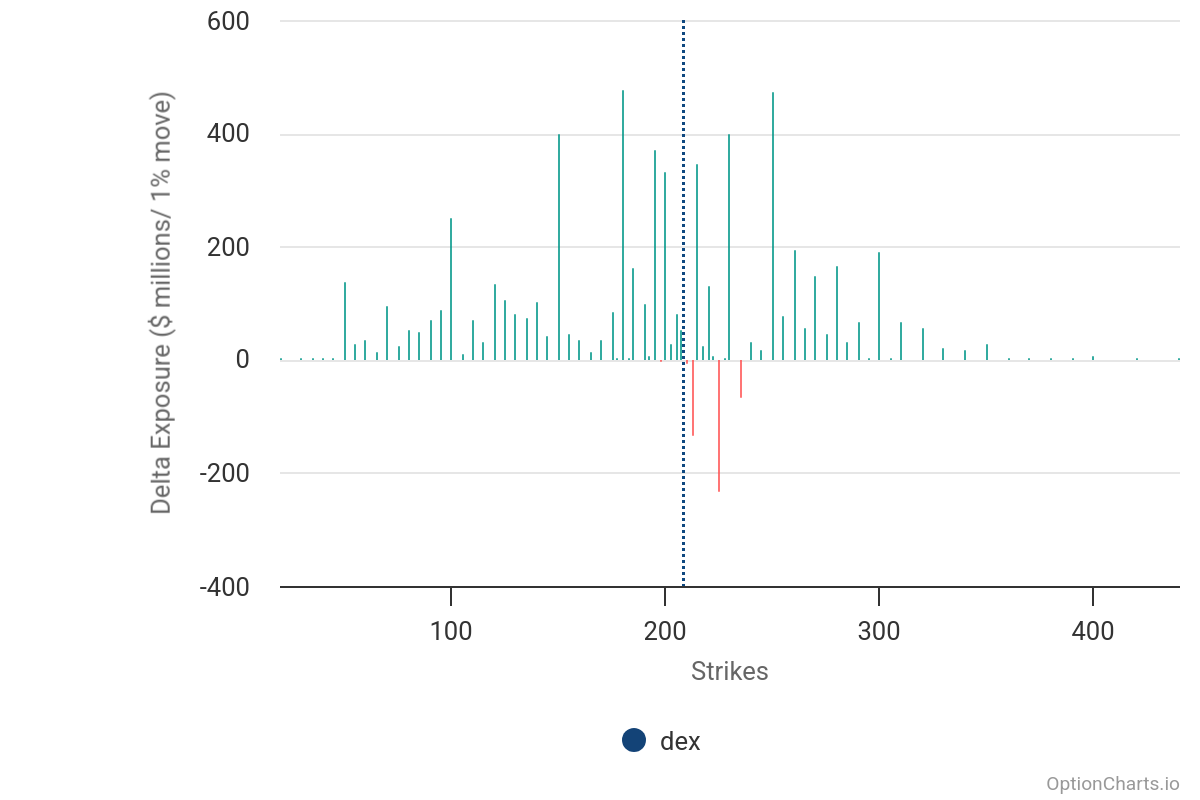

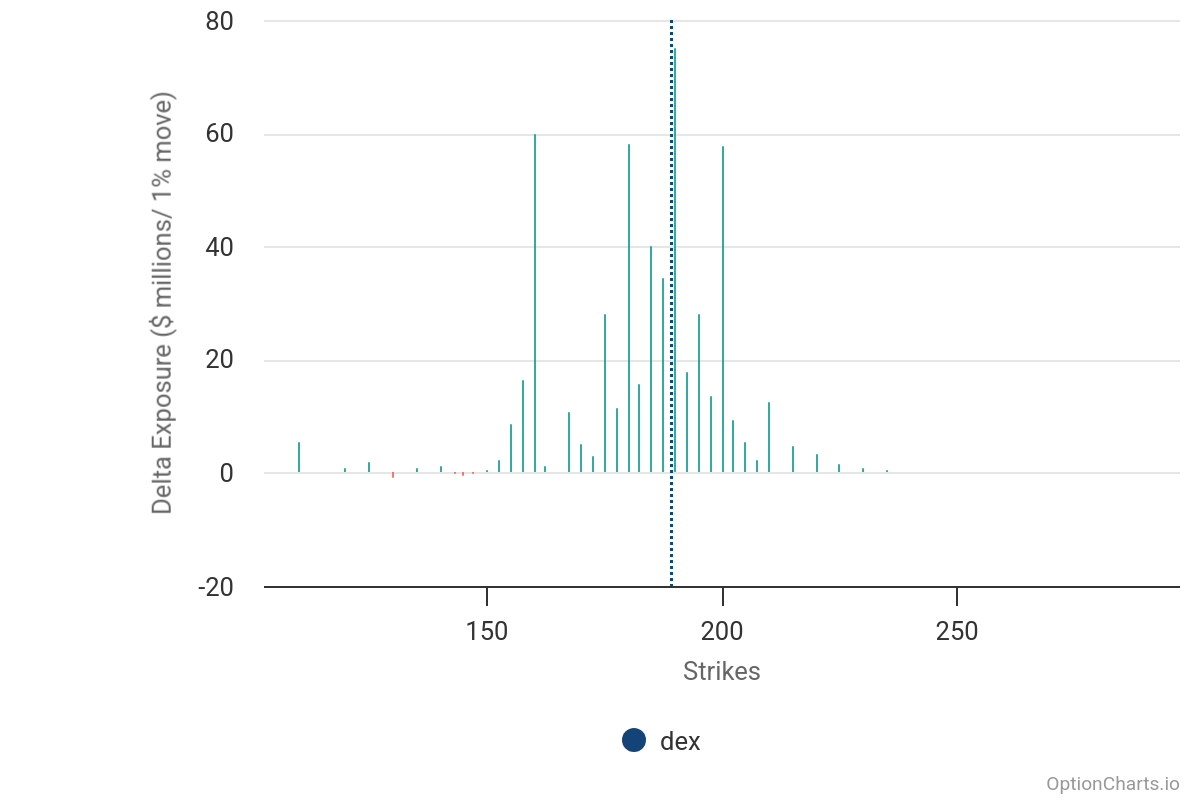

Apple, for example, has a notably large positive net delta exposure, indicating that market makers are positioned long as a hedge.

The issue is that implied volatility is unusually high for Apple, causing premiums on puts and calls to become elevated. After the company reports results, implied volatility will collapse, leaving market makers over-hedged. As a result, they’ll need to sell Apple shares to rebalance their positions. This places Apple in a situation where, regardless of earnings or guidance, the stock is likely headed lower.

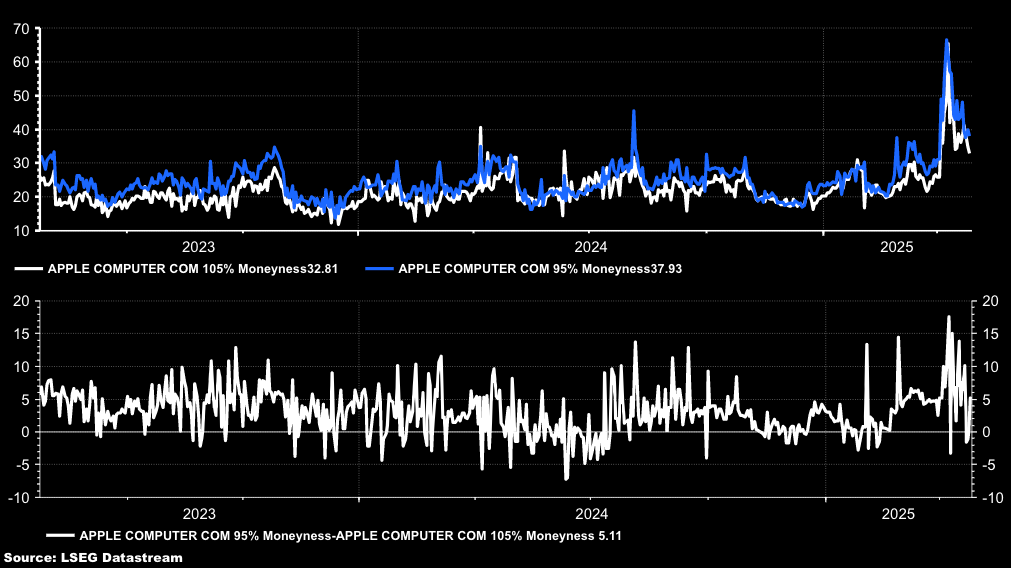

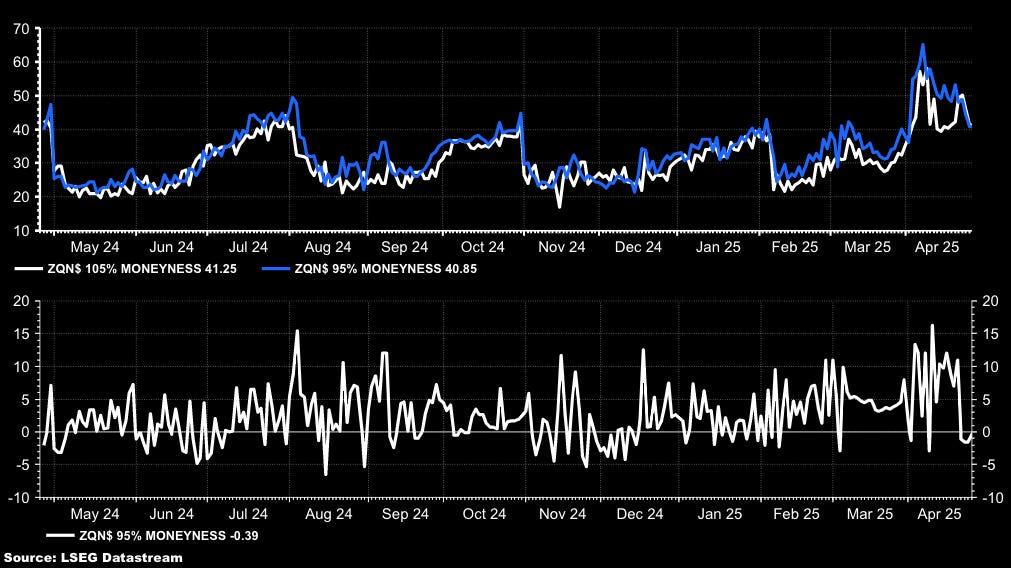

It’s the identical story for Meta as well, with very bullish options positioning heading into earnings. High implied volatility means premiums on options are elevated, and once Meta reports results, implied volatility will sharply decline. This will leave market makers over-hedged and forced to sell shares to rebalance positions, making a decline in Meta’s stock likely regardless of the earnings outcome.

In fact, Meta is arguably in an even worse position because not only is its delta positioning extremely positive, but the skew is negative. This means the 105% moneyness options are more expensive than the 95% moneyness options. Therefore, market makers aren’t just heavily hedged for an upward move—they also face more implied volatility burn-off in calls than puts. Like Apple, unless Meta delivers jaw-dropping results that surprise even the most bullish analysts, its shares are likely headed lower.

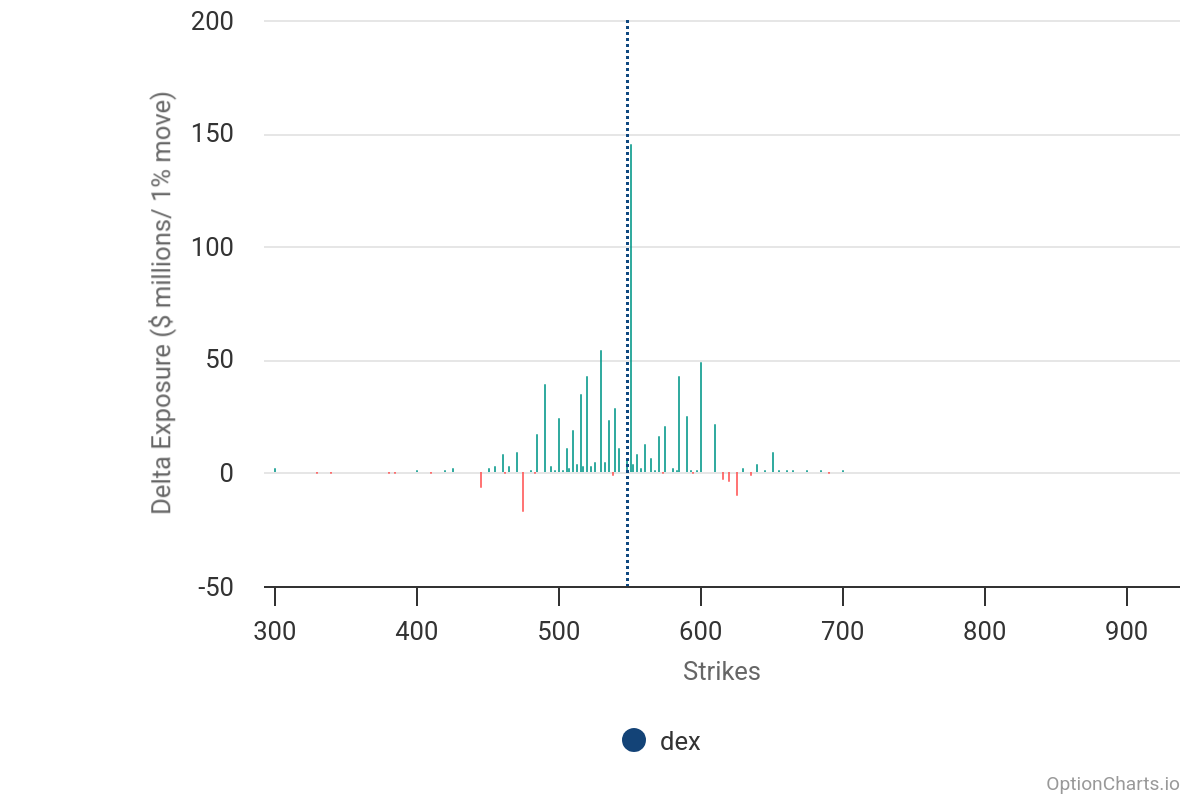

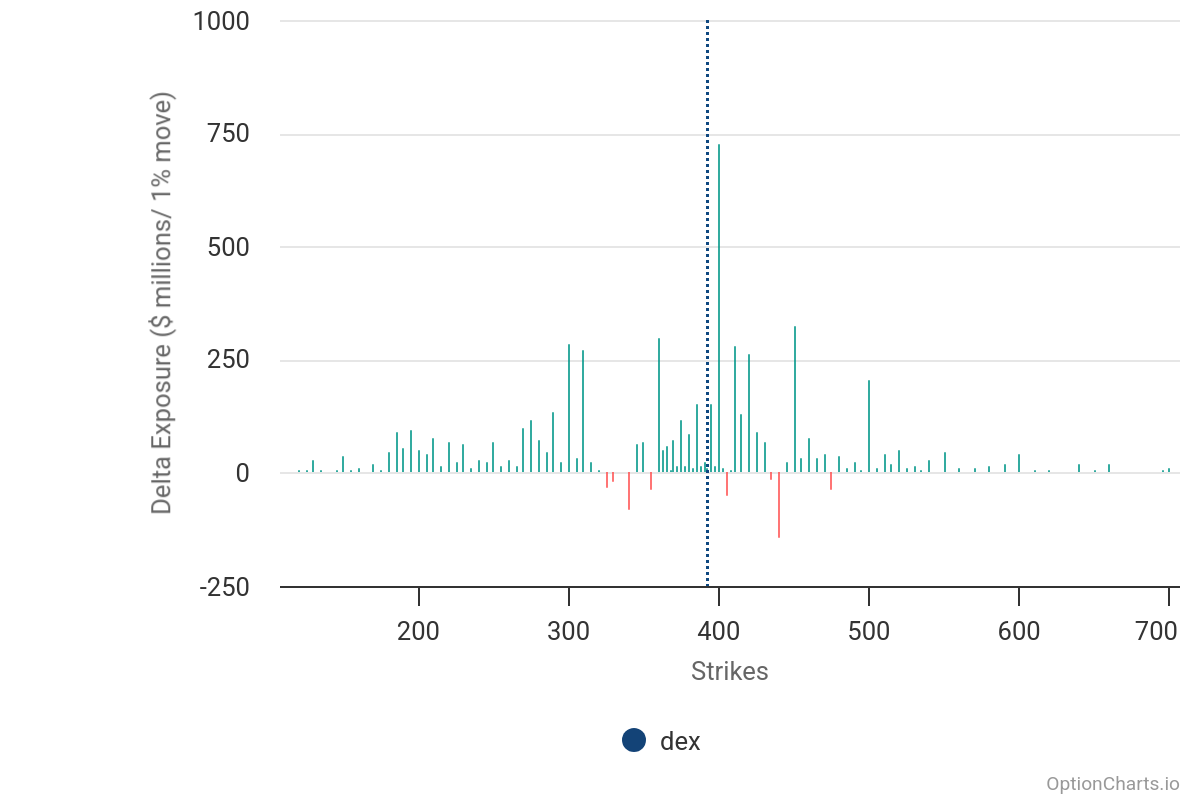

Amazon is no different from Meta or Apple, with similarly heavy positive delta positioning. Market makers are once again heavily hedged for an upward move, creating the same scenario: implied volatility will collapse after earnings, leaving market makers over-hedged and forcing them to sell shares to rebalance. This means Amazon shares, like Apple and Meta, are likely to decline after reporting results.

Also, like Meta, Amazon has a negative skew, meaning upside hedges are more expensive than downside ones. This again suggests the call options will lose value much faster than the puts after earnings, further increasing selling pressure on the stock as market makers unwind their hedges.

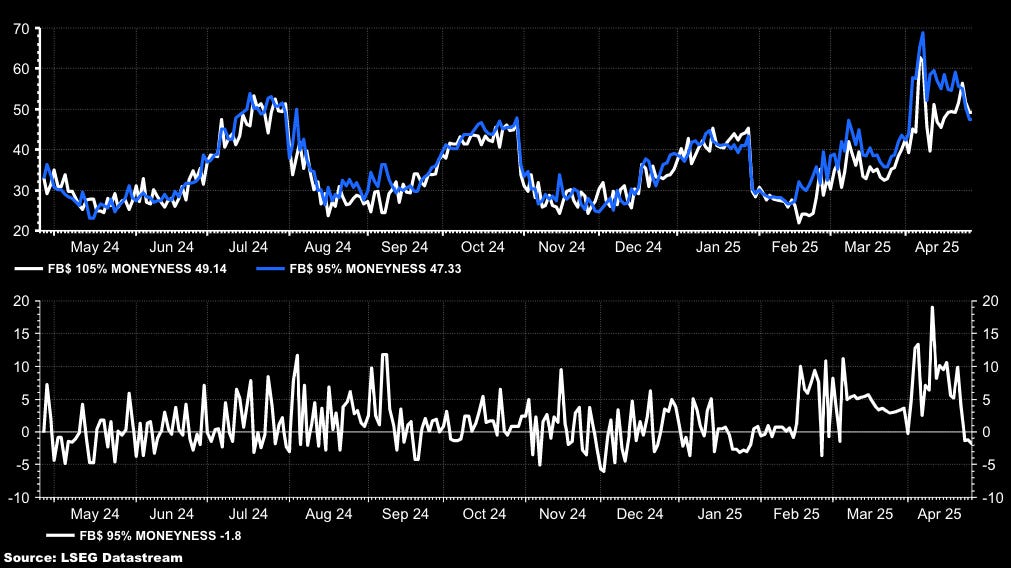

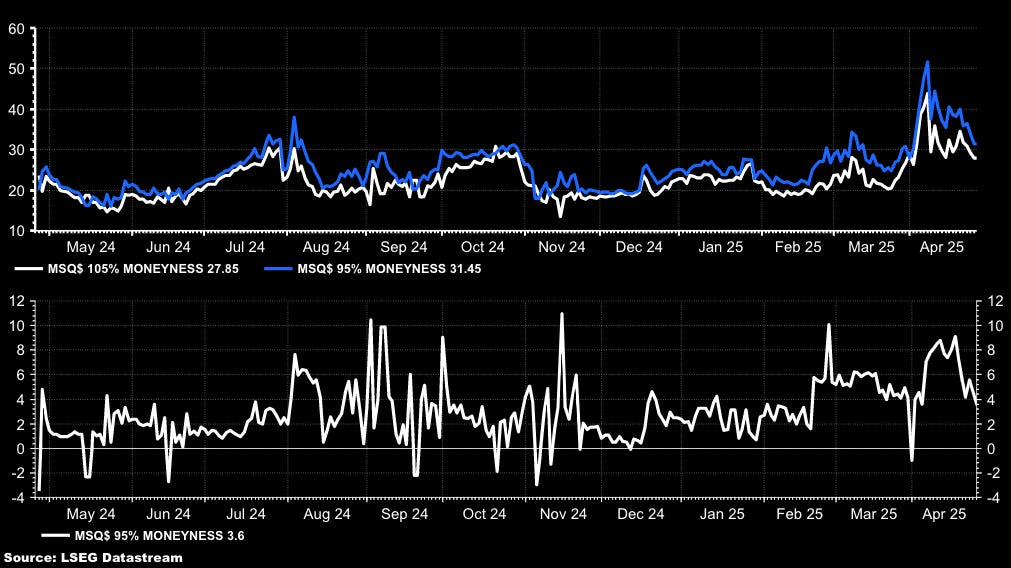

Finally, Microsoft is no different, also carrying a heavily positive delta position heading into its earnings this week. Just like Apple, Meta, and Amazon, market makers are significantly hedged for an upward move, making Microsoft’s shares similarly vulnerable to selling pressure after implied volatility collapses following the results.

However, Microsoft’s skew is positive, meaning downside implied volatility remains significantly higher than upside implied volatility. Despite this difference, it’s unlikely to matter much, given the substantial positive delta already embedded in the options market. Once implied volatility collapses after earnings, market makers will still need to unwind their hedges, likely causing selling pressure in Microsoft shares similar to Apple, Meta, and Amazon.

So, what this is really telling us is that unless these companies report spectacular earnings—meaning significantly better-than-expected results and guidance far above estimates—the odds favor their shares falling after reporting. Anything merely in-line or even slightly better than expected probably won’t be good enough.

Have a great Sunday!

-Mike

Terms By ChatGPT :

Moneyness:

The relationship between an option’s strike price and the underlying stock’s current price, indicating whether the option is in-the-money, at-the-money, or out-of-the-money.

Delta Positioning (Net Delta Exposure):

A measure of the directional exposure market makers have due to their options positions, influencing how much they must buy or sell the underlying shares to hedge their risk.

Implied Volatility (IV):

A market-derived metric that shows the expected future volatility of a stock’s price, based on current option pricing.

IV Crush:

A rapid decline in implied volatility, usually after an event like an earnings announcement, causing options prices to fall sharply.

Skew:

The difference in implied volatility levels between options at different strike prices, reflecting market expectations of upside versus downside risk.

Positive Skew:

A situation where downside options (puts) have higher implied volatility and are more expensive than upside options (calls).

Negative Skew:

The opposite scenario, where upside options (calls) have higher implied volatility and are more expensive than downside options (puts).

Over-Hedged:

A condition where market makers have too much exposure in one direction and thus must adjust their positions, typically by selling or buying shares after volatility collapses.

Speculative Earnings:

Earnings results significantly exceeding analyst expectations, considered extraordinary enough to drive substantial price moves.

This report contains independent commentary to be used for informational and educational purposes only. Michael Kramer is a member and investment adviser representative with Mott Capital Management. Mr. Kramer is not affiliated with this company and does not serve on the board of any related company that issued this stock. All opinions and analyses presented by Michael Kramer in this analysis or market report are solely Michael Kramer’s views. Readers should not treat any opinion, viewpoint, or prediction expressed by Michael Kramer as a specific solicitation or recommendation to buy or sell a particular security or follow a particular strategy. Michael Kramer’s analyses are based upon information and independent research that he considers reliable, but neither Michael Kramer nor Mott Capital Management guarantees its completeness or accuracy, and it should not be relied upon as such. Michael Kramer is not under any obligation to update or correct any information presented in his analyses. Mr. Kramer’s statements, guidance, and opinions are subject to change without notice. Past performance is not indicative of future results. Neither Michael Kramer nor Mott Capital Management guarantees any specific outcome or profit. You should be aware of the real risk of loss in following any strategy or investment commentary presented in this analysis. Strategies or investments discussed may fluctuate in price or value. Investments or strategies mentioned in this analysis may not be suitable for you. This material does not consider your particular investment objectives, financial situation, or needs and is not intended as a recommendation appropriate for you. You must make an independent decision regarding investments or strategies in this analysis. Upon request, the advisor will provide a list of all recommendations made during the past twelve months. Before acting on information in this analysis, you should consider whether it is suitable for your circumstances and strongly consider seeking advice from your own financial or investment adviser to determine the suitability of any investment.

The bullish option bets are likely primarily retail who aren't paying attention to IV, will be severely dissapointed this week.